7 Foolproof Accounting Truths Every Smart Small Business Owner Must Know

/

Accounting and bookkeeping is a mystery for many people launching businesses. Even if you’ve been operating a business for a while, you might not understand what your accountant is actually doing. (Are they casting magical spells?)

No matter where you are in your business journey, your finances don’t need to be a mystery. Let’s start at the beginning with an overview of accounting, bookkeeping, and how it all works from a high level. In later articles, I’ll get into the specifics, like how to regularly tend your finances and how to understand the financial health of your business.

Your financial accounts are a key record to keep about your business. It’s proof you can show to the IRS, banks, and anyone else who needs to know how your business is doing. Regularly tending to your finances will save you headache at tax time. Your books let you make proactive, informed decisions about the future of your business.

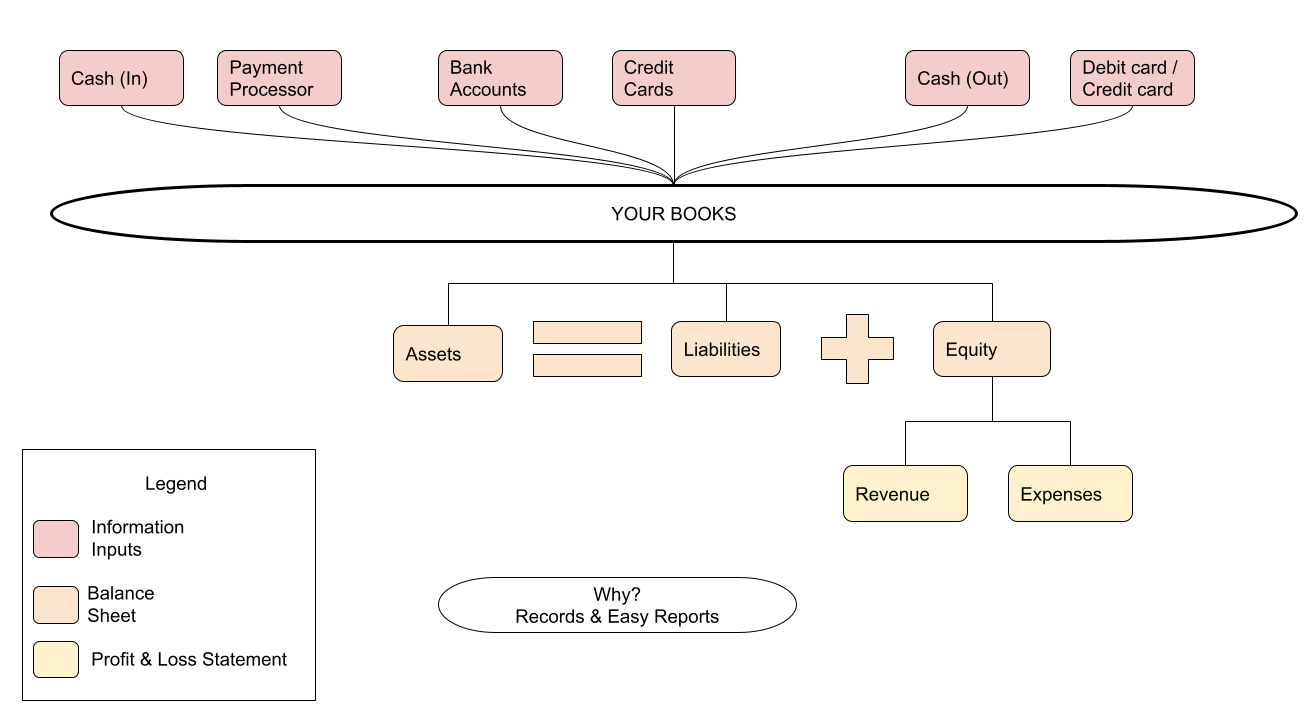

Your Books, Illustrated

Your "books" are essentially a record of all the money coming, going, and moving around in your business. This means it includes all your revenue streams, expenses, bank accounts, credit cards, cash, sales tax collected, point-of-sale system fees, unpaid invoices... EVERYTHING. All these get funneled into and (hopefully) organized into a standard format. This means that generating standard reports is super easy. It's ok if you're not familiar with these standard reports; we'll get to that soon.

Accounting 101

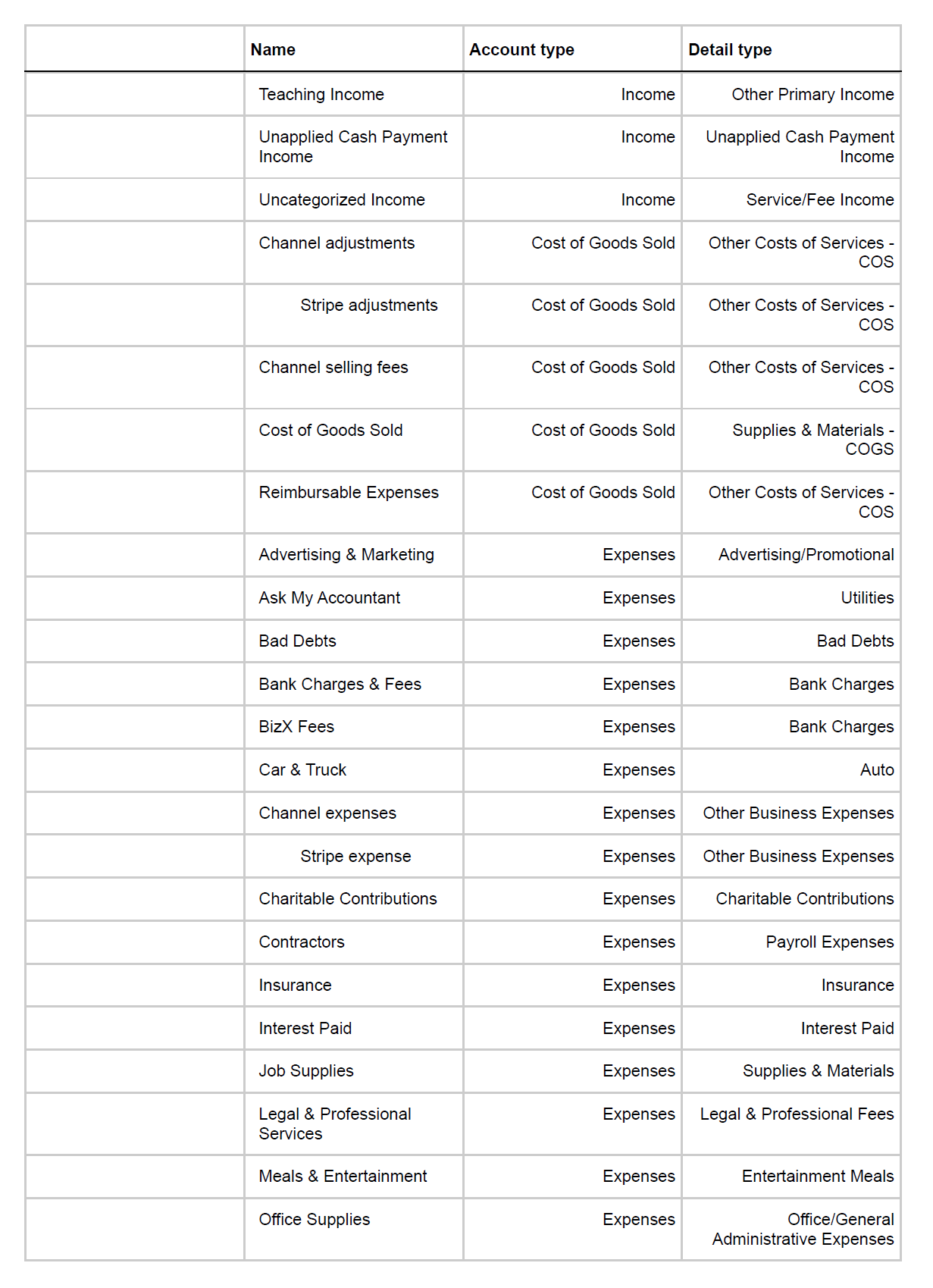

This is a small number of the accounts included in my chart of accounts

All those transactions and accounts get sorted into 5 basic types of transaction categories. These are represented in your Chart of Accounts. (Does accounting use the same words over and over again until they have no meaning? Yes. So sorry; I don't make the rules.) Your Chart of Accounts can be over-simplified into the categories for your transactions.

The primary three account types are assets, liabilities, and equity. Nestled inside equity are the final two categories: expense and income. These all relate to one another, but let’s start by defining them.

Assets

Like how you colloquially use this word, these are the valuable things you have. Most obviously, this is any cash that hangs out in your bank accounts or in your wallet. But it’s also a bunch of other things. This includes revenue you’ve invoiced but not received yet, store credit for an item you returned, and any inventory or property. If none of these happen in your business, then they won't appear in your books. But if you have some, it’ll show up as an asset in your bookkeeping.

Liabilities

Think of this as money that’s not yours or money you owe to someone else. A common example would be a balance on a credit card or a small business loan. Consider that it also includes sales tax and payroll taxes. You collect these, but the funds actually belong to the government. Some liabilities are not vital for self-employed businesses to track. For example, invoices from vendors that you’ve not yet paid are technically a liability. But the gap between receiving and paying them is small enough to be negligible. Gift certificates that you’ve sold are another potential liability. In the strictest sense, they're a liability until the recipient has redeemed them or they expire. For small volumes of gift certificates, you can get away with categorizing them as income.

Equity

This is your investment in the business and the results of your business efforts.

Let's say you put $100 of your own money in the business bank account to get started. That means you’ve made a $100 owner investment in your business. If you transfer money from the business account to your personal account, that’s called an owner draw. Both the investment and the draw are recorded, and they zero each other out.

The goal of your business is to generate more revenue than it spends. When this happens, it means you're increasing the equity. This type of equity is called retained earnings. A positive balance in retained earnings will hang out until you decide to do something with it. For self-employed businesses, your retained earnings will probably become an owner draw. (aka you're gonna pay yourself!)

The retained earnings category encompasses all the income and expense categories.

Income

These are all the ways your business earns money. The amount should be how much you receive from the customer, inclusive of any payment transaction fees, taxes, or direct costs. i.e. the grand total that you got from the customer.

For example, let's say you buy a widget for $10 and sell it to a customer for $20. Due to local sales tax laws, you have to add $2. Your payment processor then takes $0.40 as a transaction fee. In your accounts, the income recorded is $22 (the total paid by the customer). All those other numbers do reduce your income. However, they're categorized as expenses or liabilities.

In your bookkeeping, there are a few delineations that it’s important to keep clear. Income from products needs to be separate from services. Purchases of gift certificates (or other forms of client credit) also need to be in their own category. Beyond that, you can group your income streams however makes sense to you. As an example, I have separate income accounts for one-on-one coaching, group coaching, and Launch Pad subscriptions.

Expenses

This is everything your business spends money on. It doesn’t matter if it’s tax-deductible or not. Expenses include payment transaction fees, employee pay, and independent contractors' pay. It does not include owner draws. (That’s an equity account, remember?)

In your bookkeeping, it’s most important that your expense categories make sense to you. There are also categories that are nice to have since the IRS includes them in tax filings. Most accounting software starts with a Chart of Accounts that aligns with IRS filings. In case you want to be extra sure, the expense categories that the IRS cares about are the following:

Advertising

Car and truck expenses

Commissions and fees

Contract labor

Depreciation

Employee benefit programs

Insurance (other than health insurance)

Interest

Legal and professional services

Office expense

Pension and profit-sharing plans

Rent or lease (vehicles, machinery, equipment, or business property)

Repairs and maintenance

Taxes and licenses (not federal income tax!)

Travel and meals (meals are typically 50% deductible)

Utilities

Wages

Supplies

Other expenses

You do not have to spend money in each of these categories. You can also have many more categories than this. I have a dozen categories that are all a part of the IRS’s “other expense” category. They are still business expenses. Use categories that are helpful to YOU!

Standard Reports

All these account types relate to each other. Their current state appears in two standard reports: the Balance Sheet and the Profit & Loss Report, or P&L for short. Small businesses can operate just fine without being familiar with these reports. But it's a lot easier to understand your financial health with these reports.

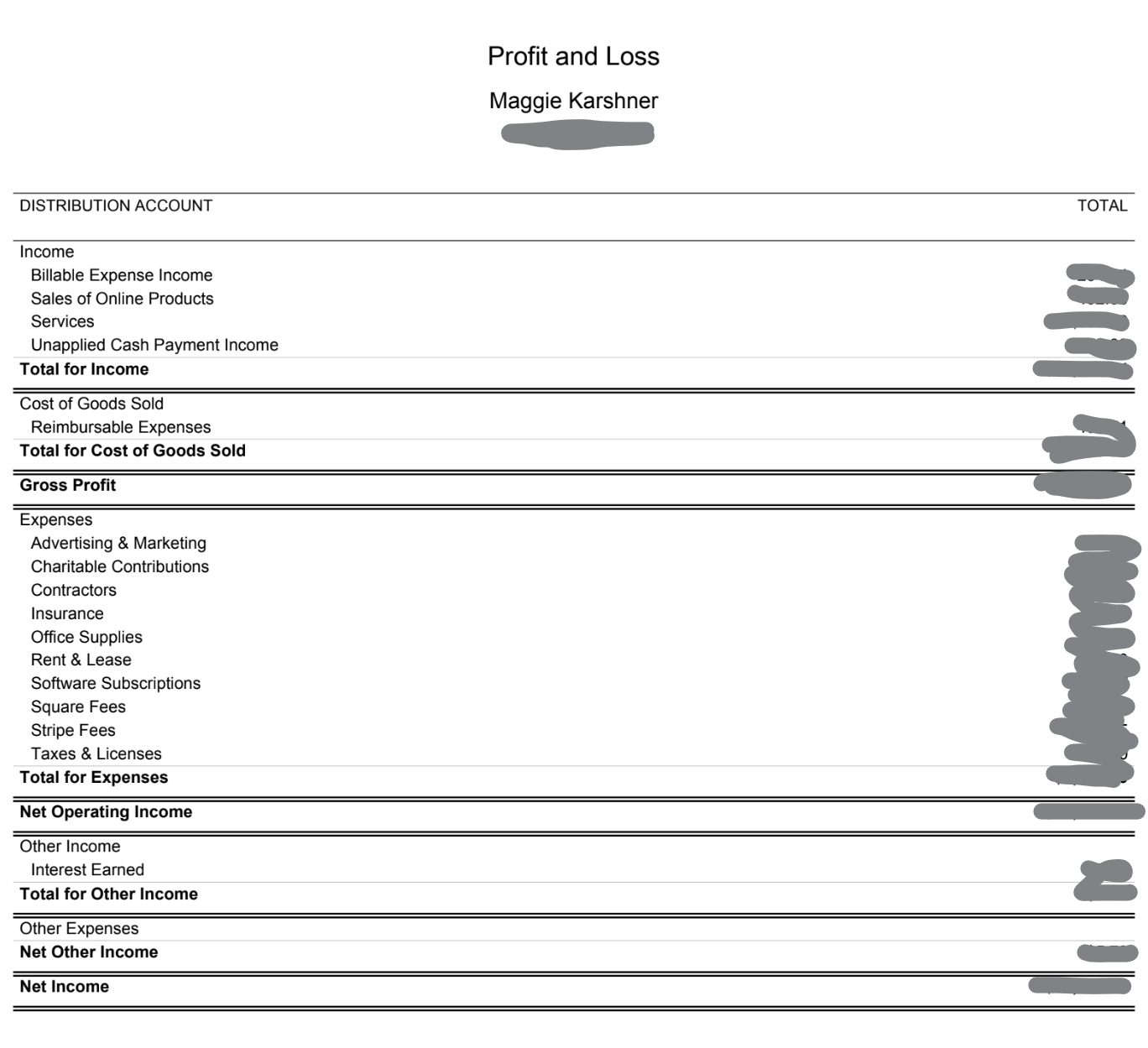

P&L’s for Beginners

This is the more interesting report for self-employed businesses. This fundamental business report shows all your income and expense accounts. All individual transactions are totaled by account. The accounts are then summed by type into a total income and total expenses. The end of this report shows the income minus the expenses. Also known as net income or profit. If it's negative, then you're taking a loss.

A P&L illuminates a few things. First off, it's a great place for a gut-check. If you look at the value for a category and think "that can't be right," follow that thought! Investigate!

This report also helps you investigate profit problems. That final number of the report is just the tip of the iceberg. Knowing that you're turning a profit or a loss doesn't help you change that situation. However, seeing that an income account is underperforming or that expenses are unexpectedly high does. Understanding these things helps you right the ship if you’re not turning a profit.

That final number on the P&L is the amount that shows up in the Retained Earnings equity account. And that shows up on your Balance Sheet …<segue>

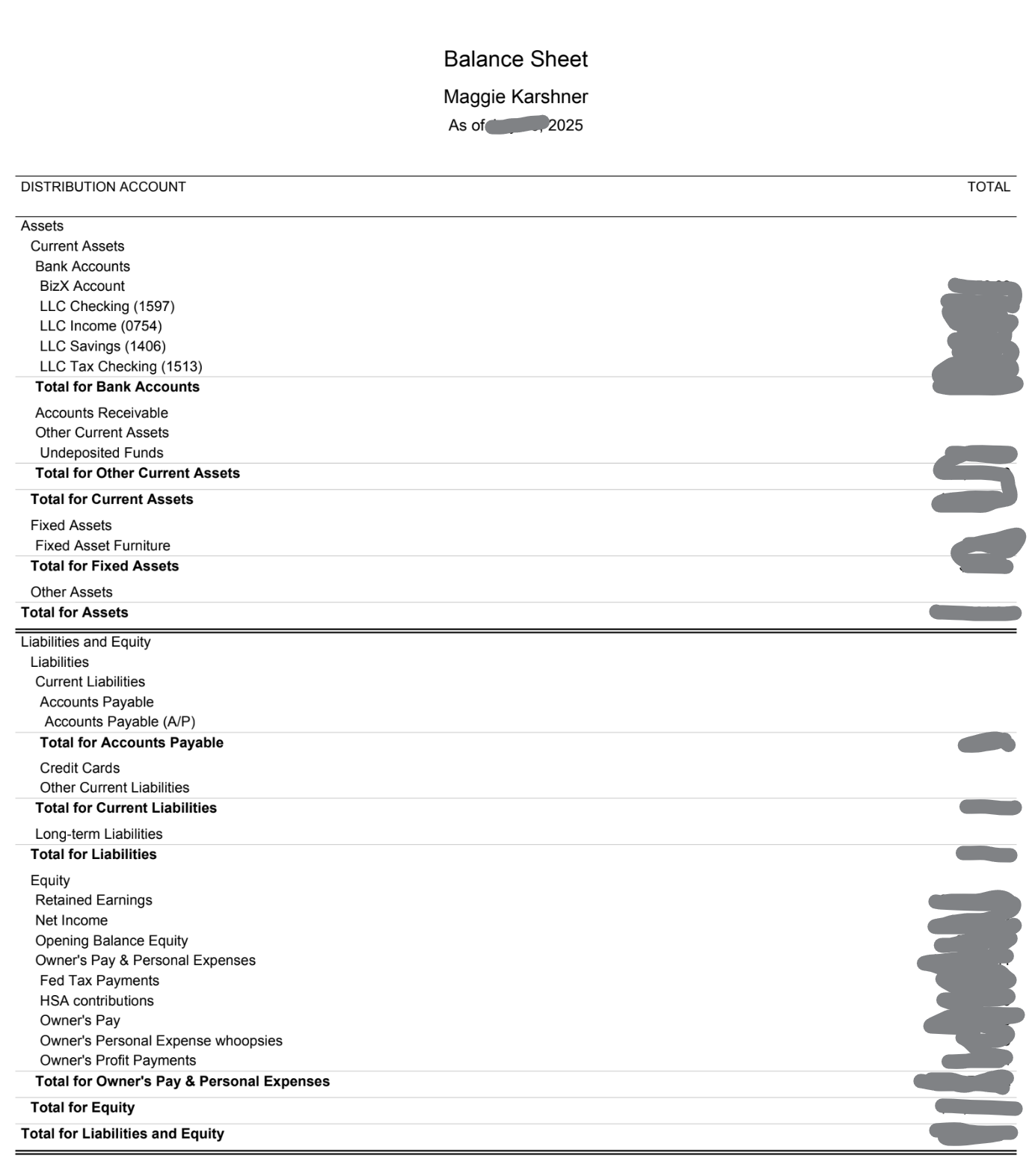

Your Balance Sheet

Don't overthink this one. This report is telling you things you already know, but in accounting-ese. Do your bank accounts have money in them? Is your credit card carrying a balance? Does your business have retained earnings or not? Your answers to these questions should match what you see on your balance sheet.

This report is a big nothing burger kinda by design. The assets always equal the liabilities plus the equity. Any accounting software worth its salt will create a balance sheet report that achieves this goal. Businesses with complex financing will have much more involved balance sheets. For self-employed businesses, your balance sheet should be pretty simple. An accounting of what’s in your bank accounts and credit cards, balanced by how much your business has brought in and how much you’ve taken out.

When you check your balance sheet, focus on the things that don't seem right. Those are signs of an accounting error, so get that fixed!

An Invitation to Go Deeper

These are just some foundational concepts, and you probably have more questions than you started with. But you also have more knowledge. You aren't in this learning journey alone! I'm here to help, as well as your accountant, tax preparer, and/or bookkeeper. (Need help finding one of these? I've got guidance in The Launch Pad!) Don’t let perfection be the enemy of done! Take your accounting bull by the horns.